HO-4 vs. HO6 Insurance: Why Condo & Co-Op Owners Need More Than a Renter's Policy

HO-4 vs. HO-6 Insurance:

Why Condo & Co-Op Owners Need More Than a Renter’s Policy

“An investment in protection pays the best interest.”

—Benjamin Franklin

If you live in a condominium or cooperative community, the insurance you carry matters far more than many owners realize — especially when a major loss impacts the entire building.

One of the most common (and costly) mistakes we see is condo or co-op owners relying on an HO-4 renter’s policy when they actually need HO-6 condo insurance.

The difference isn’t just technical. When something goes wrong, it can mean the difference between being protected — or facing thousands of dollars in unexpected costs.

Let’s break it down.

Understanding the Basics

What Is an HO-4 Policy?

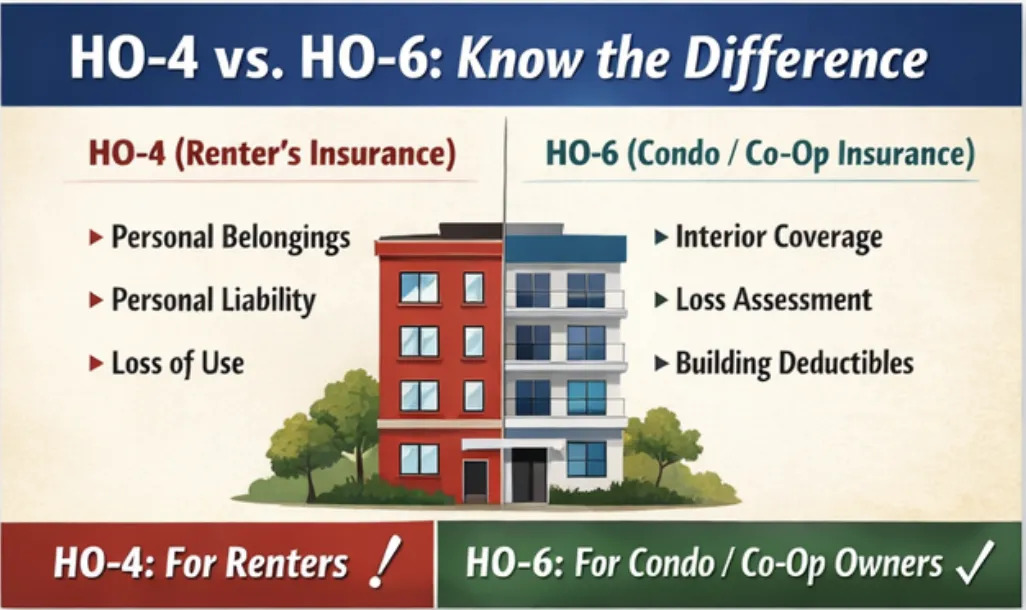

An HO-4 policy is designed for renters, not owners.

It typically covers:

Personal belongings

Personal liability

Loss of use (temporary living expenses)

What it does not cover:

The structure of your unit

Interior walls, fixtures, flooring, cabinets, or upgrades

Loss assessments from your condo or co-op association

If you own your unit, an HO-4 policy leaves serious and expensive gaps.

What Is an HO-6 Policy?

AnHO-6 policyis specifically built forcondo and cooperative owners.

It typically covers:

Personal property

Personal liability

Interior walls, flooring, cabinets, fixtures, and improvements

Loss assessment coverage

Loss of use

In short, it protects what you own and what you’re financially responsible for as part of a shared-ownership community.

What Is an HO-6 Policy?

An HO-6 policy, often referred to as condo insurance, is specifically designed for condominium and cooperative unit owners— not renters.

Unlike renter’s insurance, an HO-6 policy recognizes that while your association insures the building as a whole,you still own — and are financially responsible for — everything inside your unit and your share of certain community risks.

An HO-6 policy typically covers:

Personal Property

Protection for your belongings, including furniture, clothing, electronics, appliances, and other personal items, whether they are damaged by fire, water, theft, or other covered events.Personal Liability

Coverage if someone is injured inside your unit or if you accidentally cause damage to another unit. This can help cover legal defense costs, medical expenses, and settlements.Interior Structure & Improvements

Coverage for interior walls, flooring, cabinets, countertops, fixtures, built-ins, and any upgrades or renovations you’ve made — items that are usually excluded from the association’s master policy.Loss Assessment Coverage

One of the most critical protections for condo and co-op owners. This helps pay your share of association assessments when the master policy falls short due to deductibles, coverage limits, exclusions, or liability claims.Loss of Use

Pays for temporary housing, meals, and other living expenses if your unit becomes uninhabitable due to a covered loss.

In short, an HO-6 policy bridges the gap between what the association insures and what you personally own and owe. It protects your home, your investment, and your financial stability within a shared-ownership community — where risk, responsibility, and costs are never entirely individual.

The Big Risk: Loss Assessments After a Major Claim

This is where the difference between HO-4 and HO-6 becomes critical.

When a large loss occurs — such as a fire, hailstorm, water damage, or a liability lawsuit — the condo or co-op association files a claim on the master policy. But those master policies often come with:

High deductibles

Coverage limits

Exclusions

Coinsurance penalties

If the association’s insurance doesn’t fully cover the loss, the remaining cost is assessed back to the unit owners.

A Realistic Example

A fire causes $1.5 million in building damage

The association’s deductible is $100,000

There are 20 unit owners

Each owner could receive a $5,000 assessment— or more — due immediately.

And that’s just the deductible.

Why HO-4 Coverage Leaves Condo Owners Exposed

An HO-4 renter’s policy does not cover loss assessments.

That means:

You pay assessments entirely out of pocket

You have no coverage for interior damage to your unit

You may be out of compliance with lender or association requirements

One major claim could cost you thousands — or tens of thousands — personally

For condo and co-op owners, relying on an HO-4 policy is a dangerous mismatch.

Why Loss Assessment Coverage Matters

An HO-6 policy can include loss assessment coverage, one of the most overlooked — and most important — protections for condo and co-op owners.

Loss assessment coverage helps pay for costs that are legally assessed back to individual owners when the association’s master insurance policy falls short. This may include:

Association Insurance Deductibles

Many master policies carry large deductibles. If the association files a claim, unit owners are often responsible for their share of that deductible.Shortfalls in the Master Policy

When damage exceeds coverage limits, or certain losses are excluded, the remaining costs are commonly passed on to owners through special assessments.Liability Judgments Assessed to Unit Owners

If the association faces a liability lawsuit that exceeds its insurance coverage, owners may be assessed their portion of the judgment.Building Repairs Not Fully Insured by the Association

Some components of the building — or certain types of damage — may not be fully insured under the master policy, leaving owners financially responsible.

What makes loss assessment coverage especially powerful is its cost-to-benefit ratio. It is often relatively inexpensive to add to an HO-6 policy, yet it can protect against assessments that reach thousands — or even tens of thousands — of dollars.

This coverage is particularly valuable in:

Older Buildings, where systems and infrastructure are more likely to fail

Properties with High Deductibles, which increase owner exposure after a claim

Communities with Limited Reserve Funds, where repairs are more likely to trigger assessments

Cooperative Ownership Structures, where financial responsibility is more directly shared among residents

In shared-ownership communities, risk is never isolated. When one major loss occurs, everyone shares in the financial impact. Loss assessment coverage helps ensure that shared risk doesn’t become a personal financial setback.

Condo & Co-Op Living Requires the Right Protection

Living in a condominium or cooperative community offers shared amenities, shared responsibility, and shared risk. While your association’s master policy insures the building itself, that coverage is not complete protection for individual owners.

As a unit owner, you still carry financial exposure — for what’s inside your unit, for your share of community losses, and for costs that fall outside the association’s insurance limits.

AnHO-6 policyfills those critical gaps. It:

Completes the Coverage Puzzle

It bridges the space between the association’s master policy and your personal responsibility, ensuring there are no dangerous gaps when a claim occurs.Protects Your Personal Investment

Your unit, upgrades, and belongings represent a significant financial commitment. An HO-6 policy helps safeguard that investment from unexpected damage or loss.Shields You From Surprise Assessments

Loss assessment coverage can help absorb the financial shock of association deductibles, uncovered repairs, or liability claims assessed back to owners.Aligns With Lender and Association Requirements

Most lenders and condo or co-op associations require HO-6 coverage. Carrying the proper policy helps keep you in compliance and protects your financing.

An HO-4 renter’s policy simply doesn’t address these realities. It was never designed for ownership — and in shared-ownership communities, the wrong insurance can turn a single claim into a personal financial crisis.

Choosing the right protection isn’t just about insurance — it’s about understanding how shared ownership really works and making sure your coverage matches your responsibility.

Final Thought

If you own a condo or co-op unit, renter’s insurance is not enough — and the gaps don’t become visible until it’s too late.

A properly structured HO-6 policy with adequate loss assessment coverage is one of the smartest steps you can take to protect your home, your finances, and your peace of mind.

If you’re unsure what your association’s master policy covers — or whether your current insurance leaves you exposed — now is the time to review it.

Because in shared living communities, the biggest risks are often shared too.

Learn More with CooperativeShares.com

Understanding condo and cooperative ownership goes far beyond buying or selling a unit — it’s about knowing how shared ownership really works, including the financial responsibilities that come with it.

CooperativeShares.com is built to educate, inform, and empower buyers, owners, boards, and professionals navigating cooperative and condominium housing. From ownership structures and insurance considerations to governance, financing, and long-term value, we help make complex topics clearer and more accessible.

Whether you’re evaluating a co-op share, purchasing a condo, or already part of a shared-ownership community, learning how risk, responsibility, and protection intersect is essential.

Visit CooperativeShares.com to explore resources, listings, and insights designed specifically for cooperative and condominium living — because informed owners make stronger communities.